USDA Construction Loans: Requirements, Rates & Approved Builders

If you want to build a custom home in a rural area, a USDA construction loan may be the most affordable path available. With zero down payment, a single closing, and a loan that automatically converts into a 30-year fixed mortgage, it's one of the few programs that covers land acquisition, construction costs, and permanent financing in one shot.

This guide covers everything you need to know: how USDA construction loans work, current borrower and property requirements, how to find USDA-approved contractors by state, and how to get your USDA construction loan.

A USDA construction loan, also known as a USDA construction-to-permanent loan or USDA one-time close construction loan, is a government-backed mortgage administered through the USDA's Single-Family Housing Guaranteed Loan Program. It enables eligible borrowers (usually low- to moderate-income borrowers) finance land purchase and new home construction on that land through one loan with a single closing.

Unlike a standard USDA purchase loan, which applies to existing homes, a USDA construction loan is designed specifically for custom builds. Once construction is complete, the loan automatically converts to a standard 30-year fixed-rate USDA mortgage without having to refinance or go through another closing process.

The USDA single-close construction loan combines three financing needs into one:

Funds are released at construction milestones, typically during foundation building, framing, mechanical rough-in, and final inspection. Your lender manages disbursements and coordinates required inspections throughout.

USDA construction loan funds can be applied to:

USDA construction loans don’t cover vacation homes, investment properties, or income-producing properties are not covered. ADUs (accessory dwelling units) may be eligible under this specific program as long as it’s not designed for rental income.

| Requirement | Details |

|---|---|

| Credit score | No official USDA minimum, but most lenders a minimum 620 credit score |

| Debt-to-income ratio | Less than or equal to 41% |

| Income limit | Family income cannot exceed 115% of area median income (AMI) for your county and household size. In most counties, households of 1–4 people must earn below $119,850 per year. |

| Citizenship | Must be a U.S. citizen or eligible noncitizen |

| Primary residence | Must plan to live in the home full-time |

| Credit history | Stable 12–24 month history; no bankruptcy within the past 2 years |

The property must be:

You must:

Only USDA-approved contractors can provide builder services. Contractors must meet specific financial, licensing, and experience criteria, according to USDA guidelines.

USDA-approved contractors must:

Since USDA construction loans allow for no-down payment financing, the USDA requires approved contractors to ensure the home is built properly and within budget. Working with an experienced and USDA-compliant builder reduces risks for both the borrower and the lender.

If you're considering a USDA construction loan, your lender can provide a list of approved contractors.

If you're considering a USDA single-close construction loan, here are the steps you should follow to increase your chances of approval and ensure a smooth experience.

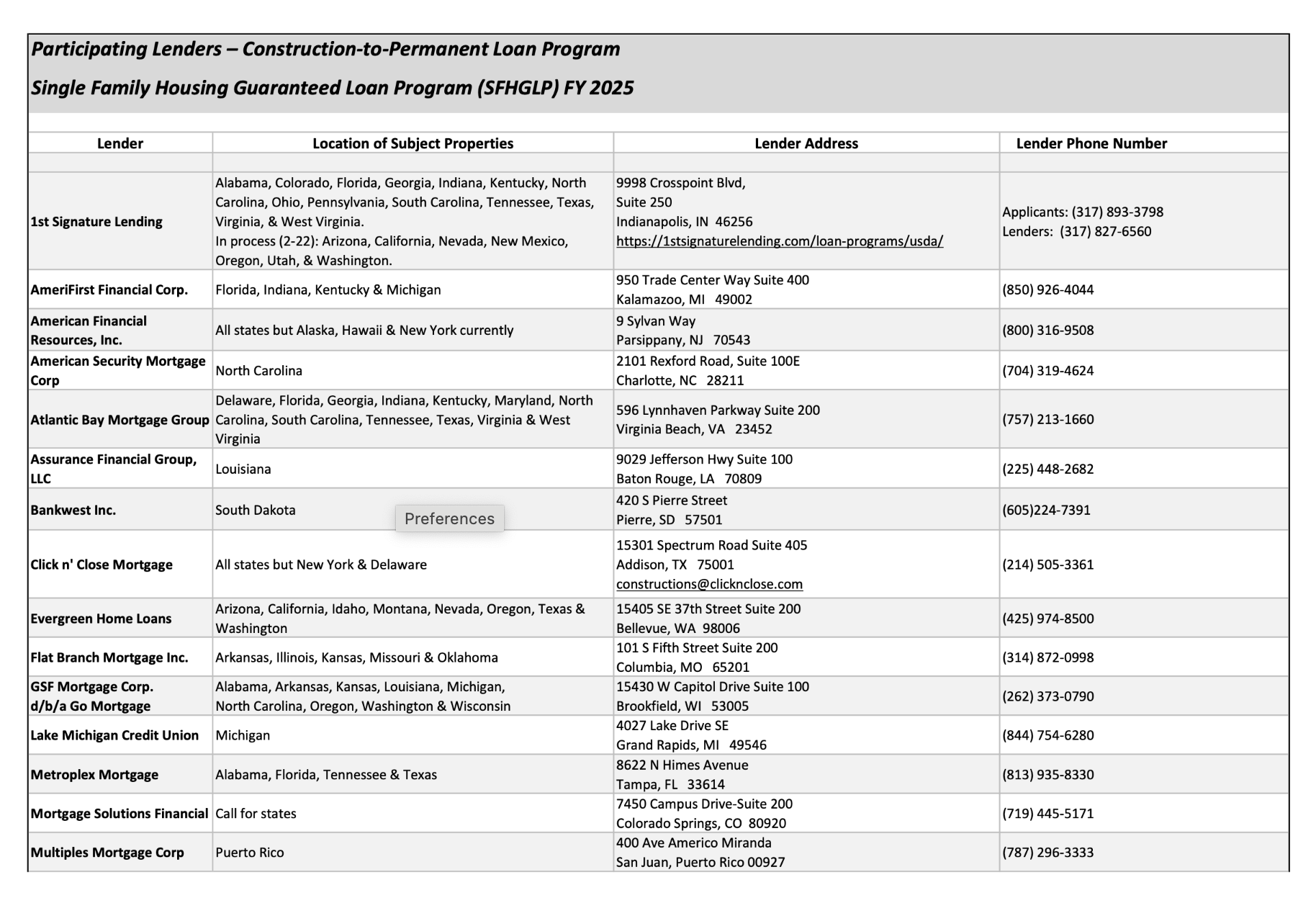

The first step is to find lenders that offer USDA construction loans. Compare the services, interest rates, and fees from several lenders to find the best match for your financial situation.

Get prequalified by meeting your lender’s requirements for the loan.

The next step is to choose a USDA-approved contractor or builder.

Your lender may provide a list of approved contractors, or you can contact the USDA directly for recommendations. Ensure your chosen contractor has experience completing projects that meet USDA regulations.

Next, secure a plot of land in an eligible area for USDA financing. USDA loans are intended to promote development in rural areas, so the land must meet certain location requirements to qualify for a USDA construction loan.

Visit our interactive USDA eligibility map to help determine if your area meets the rural requirement.

Finally, develop a construction plan with your contractor and submit your loan application to your lender with your detailed construction plan. After reviewing all documents, your lender will send it to the USDA to approve it.

| State | Builder Name | City | Website | Contact Info |

|---|---|---|---|---|

| Alabama | America’s Home Place | Dothan, AL (multiple AL offices) | americashomeplace.com | (334) 836-1216 |

| Alabama | Trinity Custom Homes | Cullman, AL | trinitycustom.com | (256) 737-5055 |

| Alaska | Spinell Homes | Anchorage, AK | spinellhomes.com | (907) 344-5678 |

| Alaska | Hall Quality Homes | Palmer, AK | hallqualityhomes.com | (907) 746-2757 |

| Arizona | Adair Homes | Phoenix, AZ | adairhomes.com | (480) 605-6205 |

| Arizona | Morgan Taylor Homes | Scottsdale, AZ | morgantaylorhomes.com | (480) 626-1555 |

| Arkansas | United Built Homes | Little Rock, AR (statewide AR) | ubh.com | (877) 756-2525 |

| Arkansas | Rausch Coleman Homes | Fayetteville, AR | rauschcolemanhomes.com | (479) 455-9090 |

| California | G.J. Gardner Homes | Sacramento, CA | gjgardner.com | (916) 471-4141 |

| California | Element Homes (Construct Elements) | Los Angeles, CA | constructelements.com | (310) 516-5161 |

| Colorado | G.J. Gardner Homes | Colorado Springs, CO | gjgardner.com | (719) 495-2670 |

| Colorado | Journey Homes | Greeley, CO | journeyhomes.com | (970) 356-5000 |

| Connecticut | Connecticut Valley Homes (CT has fewer rural builders – many use modular contractors like above) | East Lyme, CT | ctvalleyhomes.com | (860) 739-6913 |

| Delaware | Beracah Homes | Greenwood, DE | beracahhomes.com | (302) 349-4561 |

| Delaware | Insight Homes | Bridgeville, DE | insighthomes.com | (302) 337-0400 |

| Florida | America’s Home Place | Gainesville, FL | americashomeplace.com | (352) 244-8442 |

| Florida | Maronda Homes | Sanford, FL | marondahomes.com | (866) 577-6675 |

| Georgia | America’s Home Place | Gainesville, GA | americashomeplace.com | (770) 536-9852 |

| Georgia | Trinity Custom Homes | Ellijay, GA | trinitycustom.com | (888) 818-0278 |

| Hawaii | Honsador Homes | Kapolei, HI | honsador.com | (808) 682-2011 |

| Hawaii | Hawai‘i Island Community Dev. Corp. | Hilo, HI | hicdc.org | (808) 969-1158 |

| Idaho | HiLine Homes | Star, ID | hilinehomes.com | (208) 231-2204 |

| Idaho | Adair Homes | Coeur d’Alene, ID | adairhomes.com | (208) 618-0901 |

| Illinois | Homeway Homes | Goodfield, IL | homewayhomes.com | (309) 965-2312 |

| Illinois | Taylor Homes | Also serves IL (office in Evansville, IN) | taylorhomes.com | (502) 955-7164 |

| Indiana | Davis Homes | Indianapolis, IN (Statewide IN) | davishomes.com | (317) 548-4663 |

| Indiana | Taylor Homes | Indianapolis, IN (Southern IN) | taylorhomes.com | (502) 955-7164 |

| Iowa | Jerry’s Homes | Des Moines, IA (Central IA) | jerryshomes.com | (515) 512-5716 |

| Iowa | Habitat for Humanity | (Various IA counties) | habitat.org | n/a (local affiliates) |

| Kansas | Wardcraft Homes | Clay Center, KS | wardcraft.com | (785) 632-5622 |

| Kansas | Prairie View Construction | Wichita, KS | (316) 312-1234 | |

| Kentucky | America’s Home Place | Bowling Green, KY | americashomeplace.com | (270) 418-2652 |

| Kentucky | Taylor Homes | Louisville, KY | taylorhomes.com | (502) 955-7164 |

| Louisiana | America’s Home Place | Baton Rouge, LA | americashomeplace.com | (225) 590-5070 |

| Louisiana | United Built Homes | Shreveport, LA | ubh.com | (877) 756-2525 |

| Maine | Coastline Homes of Maine | Ellsworth, ME | coastlinehomesofmaine.com | (207) 667-0664 |

| Maine | Maple Leaf Homes | Presque Isle, ME | carusohomes.com | (207) 764-6336 |

| Maryland | Caruso Homes | Crofton, MD | beracahhomes.com | (301) 261-0277 |

| Maryland | Beracah Homes | Denton, MD | beracahhomes.com | (302) 349-4561 |

| Massachusetts | Kozyra Construction | Brimfield, MA | kozyraconstruction.com | (413) 245-4402 |

| Massachusetts | Avalon Building Systems | Canton, MA | avalonbuildingsystems.com | (781) 294-0224 |

| Michigan | Allen Edwin Homes | Portage, MI | allenedwin.com | (269) 210-2124 |

| Michigan | Next Modular | Niles, MI | nextmodular.com | (574) 334-9590 |

| Minnesota | Dynamic Homes | Detroit Lakes, MN | dynamichomes.com | (218) 847-2611 |

| Minnesota | Bigelow Homes | Twin Cities, MN | bigelowhomes.net | (952) 447-4600 |

| Mississippi | America’s Home Place | Jackson, MS | americashomeplace.com | (601) 853-5020 |

| Mississippi | Elliott Homes | Gulfport, MS | myelliotthome.com | (844) 289-3554 |

| Missouri | United Built Homes | Springfield, MO | ubh.com | (877) 756-2525 |

| Missouri | McBride Homes | St. Louis, MO | mcbridehomes.com | (636) 537-2000 |

| Montana | Hamel Construction | Billings, MT | hamelconstruction.com | (406) 252-1325 |

| Montana | Montana Modular Homes | Belgrade, MT | mtmodular.com | (406) 388-5486 |

| Nebraska | Heritage Homes | Wayne, NE | heritagehomesofne.com | (402) 375-4770 |

| Nebraska | Hoppe Homes | Lincoln, NE | hoppehomes.com | (402) 937-4818 |

| Nevada | Braemar Construction | Elko, NV | homesbybraemar.com | (775) 777-2949 |

| Nevada | Prestige Custom Homes | Carson City, NV | prestigechomesllc.com | (775) 297-5485 |

| New Hampshire | Avalon Building Systems | Serves NH statewide | avalonbuildingsystems.com | (781) 294-0224 |

| New Hampshire | LaMontagne Builders | Bedford, NH | lamontagnebuilders.com | (603) 668-7933 |

| New Jersey | Schaeffer Homes | Cape May Courthouse, NJ | schaefferhomes.com | (856) 208-5124 |

| New Jersey | Builder’s Trading Co | Toms River, NJ | builderstrading.com | (732) 240-5540 |

| New Mexico | Hakes Brothers | Las Cruces, NM | hakesbrothers.com | (575) 521-0868 |

| New Mexico | Tierra del Sol Housing | Las Cruces, NM | tdshc.org | (575) 882-3554 |

| New York | Hudson Valley Home Source | Modena, NY | hvhomes.com | (845) 564-2977 |

| New York | Future Homes of NY | Oneonta, NY | futurehomesny.com | (607) 432-8453 |

| North Carolina | America’s Home Place | Greenville, NC | americashomeplace.com | (252) 353-8838 |

| North Carolina | Value Build Homes | Sanford, NC | valuebuildhomes.com | (919) 777-0393 |

| North Dakota | Verity Homes | Bismarck, ND | verityhomes.com | (701) 354-2988 |

| North Dakota | Schommer Construction | Dickinson, ND | schommerconstruction.com | (701) 483-1706 |

| Ohio | Wayne Homes | Uniontown, OH | waynehomes.com | (330) 893-7601 |

| Ohio | America’s Home Place | Cincinnati, OH | americashomeplace.com | (513) 800-2565 |

| Oklahoma | United Built Homes | Tulsa, OK | ubh.com | (877) 756-2525 |

| Oklahoma | Ideal Homes | Norman, OK | idealhomes.com | (405) 366-0000 |

| Oregon | Adair Homes | Bend, OR | adairhomes.com | (541) 318-3511 |

| Oregon | HiLine Homes | Redmond, OR | hilinehomes.com | (541) 923-6607 |

| Pennsylvania | S & A Homes | State College, PA | sahomebuilder.com | (855) 724-6637 |

| Pennsylvania | Schaeffer Homes | Philadelphia, PA | schaefferhomes.com | (856) 208-5124 |

| Rhode Island | Connecticut Valley Homes | Westerly, RI | ctvalleyhomes.com | (860) 739-6913 |

| Rhode Island | Millbrook Modular Homes | Worcester, MA | millbrookhomes.com | (508) 476-1500 |

| South Carolina | America’s Home Place | Columbia, SC | americashomeplace.com | (803) 776-1593 |

| South Carolina | Value Build Homes | Spartanburg, SC | valuebuildhomes.com | (864) 310-5850 |

| South Dakota | Clark Drew Construction | Brookings, SD | clarkdrewconstruction.com | (605) 696-3200 |

| South Dakota | Standing Rock CDC | Fort Yates, SD | standingrockcdc.org | (701) 854-8687 |

| Tennessee | America’s Home Place | Knoxville, TN | americashomeplace.com | (865) 938-4678 |

| Tennessee | Ole South Homes | Murfreesboro, TN | olesouth.com | (615) 219-5644 |

| Texas | Tilson Homes | Houston, TX | tilsonhome.com | (888) 540-6705 |

| Texas | United Built Homes | Lufkin, TX | ubh.com | (877) 756-2525 |

| Utah | Ivory Homes | Salt Lake City, UT | ivoryhomes.com | (801) 747-7000 |

| Utah | Self-Help Homes | Provo, UT | selfhelphomes.org | (801) 375-2205 |

| Vermont | Huntington Homes | Montpelier, VT | huntingtonhomesvt.com | (802) 433-6285 |

| Vermont | Vermod Homes | Hartford, VT | vermodhomes.com | (802) 672-5242 |

| Virginia | Mitchell Homes | Richmond, VA | mitchellhomesinc.com | (804) 261-0200 |

| Virginia | America’s Home Place | Roanoke, VA | americashomeplace.com | (540) 389-5468 |

| Washington | Adair Homes | Vancouver, WA | adairhomes.com | (360) 448-6050 |

| Washington | HiLine Homes | Puyallup, WA | hilinehomes.com | (253) 840-5660 |

| West Virginia | Panhandle Homes of BC | Martinsburg, WV | panhandlehomeswv.com | (304) 263-3100 |

| West Virginia | Almost Heaven Habitat | Franklin & Pendleton Co., WV | ahhabitat.org | (304) 358-7642 |

| Wisconsin | Wausau Homes | Wausau, WI | wausauhomes.com | (715) 848-5511 |

| Wisconsin | Timberlake Builders | Hayward, WI | timberlakebuildersinc.com | (715) 634-4505 |

| Wyoming | Tri Mountain Homes | Cheyenne, WY | trimountainhomes.com | (307) 514-0840 |

| Wyoming | Mountain View Builders | Cody, WY | mountainviewbuilders.com | (307) 587-5095 |